Evaluating the Effectiveness of the Audit Process

Internal audit activities have an important role to play within public and private sector organizations and are a core element of good governance in any size of business. There are many benefits of performance measurement for the internal audit activity, including providing objective data for improvement through self-evaluation and/or benchmarking, increasing the effectiveness and efficiency of the work, demonstrating the value internal audit brings to an organization and its management, and helps gain credibility, objectivity, and accountability of the internal audit function.

Evaluating the audit process and KPIs is a wide-scoped process, including several stages. This article presents a holistic view of the audit process evaluation, describing two important parts of this process especially applicable for organizations and corporates where internal audit is solidly established in the company functions; we will explore here: the audit process assessment from one side and the KPIs assessment from another side.

First: Audit Process Assessment:

Evaluation Metrics Considerations for a Balanced Scorecard:

Expectations of the internal audit vary widely among organizations- therefore, we can say there is no single set of best practice metrics. That said, the heads of organizations, in collaboration with internal audit teams, follow common guidelines to set their KPIs and evaluation metrics in relevance to the strategic goals and objectives of their organizations.

One of these common guidelines and standards to derive the audit evaluation metrics is the Balanced Scorecards. It is used by organizations wishing to evaluate the performance of different sides of the business functions and report back holistically in order to demonstrate interdependencies. It is a widely used strategic performance management framework that allows organizations to identify, manage, and measure their strategic objectives.

As metrics are identified across the balanced scorecard, careful consideration should be made to cover all the relevant aspects of the audit process.

According to a PwC 2014’s State of Internal Audit Profession Study, a model of the internal audit operating continuum was developed, classifying the effectiveness of the internal audit process of organizations into four levels:

– Assurance provider (basic level) – where internal audit delivers assurance of the effectiveness of internal audit,

– Problem solver – where the internal audit brings analysis on root causes of issues identified in the audit findings,

– Insight generator – where a more proactive role is taken, suggesting improvement measures to risk assurance,

– Trusted advisor (most advanced) – which provides value-added services and strategic advice to the business beyond the effective execution of the audit plan.

According to the depth of scope of the performance indicators developed, the effectiveness of the audit process is determined. The following table shows how to develop a balanced scorecard for the effectiveness of the audit plan. It also shows how the different sets of performance indicators developed can upgrade the organization across the continuum identified above. The full list of references supporting the development of this balanced scorecard and the associated performance indicators can be accessed here.”

(the lighter color shows the basic levels (Assurance provider) while the darker color shows advanced levels of internal audit effectiveness).

Second: KPIs Assessment:

The main objective of performance indicators is to assist in the development of policies. The concept of performance indicators involves the application of the combination of an analysis and decision-making model based on “achieving goals” and the principles of “causal” cause-effect relationships. KPIs give information on the results achieved by programs and strategies. To determine whether each KPI is appropriate, it must be evaluated along with the goal associated with it.

Types of Audits as per the international standards:

Standard 1300 – Quality Assurance and Improvement Program requires the chief audit executive to maintain and develop a quality assurance and improvement program. This program must cover all aspects of internal audit activities while assessing both the efficiency and effectiveness of the internal audit activity and includes both internal and external assessments:

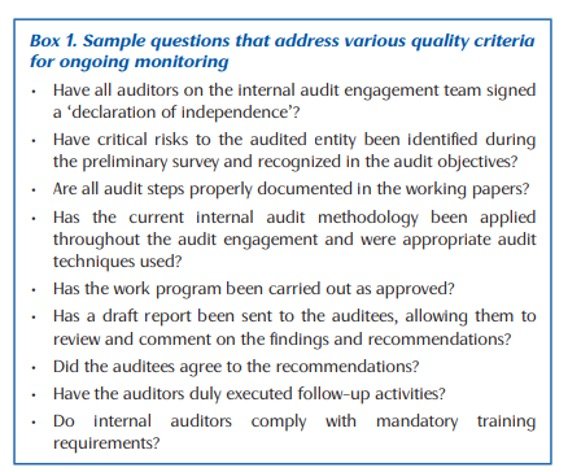

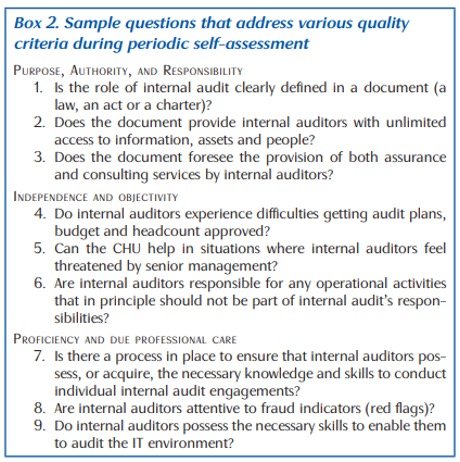

– Internal Assessments: Attribute standard 1311 requires that internal assessments should include (i) ongoing monitoring of the performance of the internal audit activity, which is part of the day-to-day supervision, review, and measurement of the internal audit activity, and (ii) a periodic self-assessments or assessments by other persons within the organization with sufficient knowledge of internal audit practices. The boxes below show sample indicators (questions) in each of the ongoing and periodic self-assessment processes. The full lists can be accessed here.

|

|

– External Assessments: Standard 1312 requires external assessments of the internal audit activity to be conducted once every five years, at least by a qualified independent assessor, and these can be in the form of a full external assessment or a self-assessment with independent external validation. The full list of questions can be accessed here.

Auditors revise each KPI and evaluate it according to the following nine criteria and score it on an X-point scale:

Relevance: Does the KPI contribute to the results that users use to make decisions?

Focused: Does the key performance indicator address an important aspect of the program’s objective? The performance indicator should help tremendously in knowing the extent to which the goal of the program has been achieved.

Understandable: Does the KPI provide sufficient information clearly and concisely? The KPI must be stated in clear language, and the results of the program must be indicated to provide information to users.

Measurable: Is it possible to measure KPIs (allowing results to be measured to illustrate overall trends over time)?

Unbiased (objective): Are the key performance indicators neutral, and are their goals to measure progress and not reach a result that improves the image of management?

Adequacy: One or more indicators must be determined for each goal or program to measure the totality and weights of varying progress toward the objective.

Completeness and accuracy of disclosures: The target number can be reached through the implementation of planned programs, projects, objectives, and activities.

Specified Timeframe: There is a specific time limit for achieving the targets.

Reliable: The indicator must be consistent and fixed for the program during the implementation of the plan and based on reference values (base year) with the possibility of making benchmarks.

The Chartered Professional Accountants of Canada developed a ready-to-use downloadable KPI Review Matrix that can be used as a guide to evaluate the KPIs used. This can be downloaded here.

Here, we will discover Common Challenges in Evaluating Audit Effectiveness:

Evaluating the effectiveness of the audit process is a difficult task with some surrounding common challenges, such as the limited staff resources and budget constraints, the complexity of conducting multiple audits, the need for consolidating efforts, the need for manual evidence collection, the need for a modern developed platform with the latest tools, and most importantly the need for an expert audit partner.

Against the above challenges, choosing the right expert partner is a premium solution to most challenges. If you’re looking for a single-provider approach and an efficient, high-quality audit experience, Ahmed Mamdouh & Co. Kreston is here to help. Our experts will guide you through your assessment journey while helping you get the most out of the audit process.

References:

https://www.ab.gov.jo/ebv4.0/root_storage/en/eb_list_page/guidlines_on_auditing_performanc_indecators.pdf

https://documents1.worldbank.org/curated/fr/840271546848703532/pdf/Internal-Audit-Key-Performance-Indicators.pdf

https://www.sciencedirect.com/topics/economics-econometrics-and-finance/balanced-scorecard

https://www.pempal.org/sites/pempal/files/knowledge_product/pempal_iacop_quality_assessment_guide_eng.pdf

https://www.corporatecomplianceinsights.com/wp-content/uploads/2014/09/PWC-press-release-9-23-14.pdf

https://www.cpacanada.ca/business-and-accounting-resources/strategy-risk-and-governance/corporate-governance/publications/kpis-a-tool-for-audit-committees

https://www.pwc.com/m1/en/publications/documents/pwc-state-of-the-internal-audit-profession-2014.pdf